I come across a lot of ridiculous things in the 403(b), but some things rate off the chart, a real WTF event or moment. That's why I'm creating a new segment on the blog titled

"Wait, That's Legal?".

In this first edition of WTL I'm going to focus on a situation that should be illegal. In fact, when I tell people about it they almost always come back with "wait, that's legal?" (yes, I'm very creative with my titles).

My wife's school district offers a Section 125 plan. For those not familiar, this is a plan that allows an employee to defer money pre-tax to be used for qualified medical expenses and for qualified child care. Not only is the money taken out of the paycheck on a pre-tax basis, if used for qualified expenses it is not taxed when withdrawn. It's tough to find a pre-tax and tax-free benefit and we use ours every year.

The administrator of my wife's plan is an insurance company, American Fidelity (yes, I've written about this before). It turns out that American Fidelity runs the Section 125 plan for free, meaning they don't charge the district for their services. Running a Section 125 is not cheap, so how is it that American Fidelity can do it for nothing? Coercion.

Most Americans have their health insurance premiums paid for out of their paycheck. The advantage is that if paid through a paycheck, the premiums come out pre-tax for both State and Federal taxes (it might vary on the State level). This is a perk of the tax code and one need not do anything to receive...unless of course you are an employee in my wife's school district (or other American Fidelity plans that are run in a similar fashion).

In my wife's school district every employee is assumed to NOT want their health care insurance premiums taken out pre-tax. If they want this "perk" they are forced to meet with an insurance agent from...American Fidelity. When they meet with that agent they are in a room with just that agent and the agent attempts to sell the employee any number of needless insurance policies and 403(b) products.

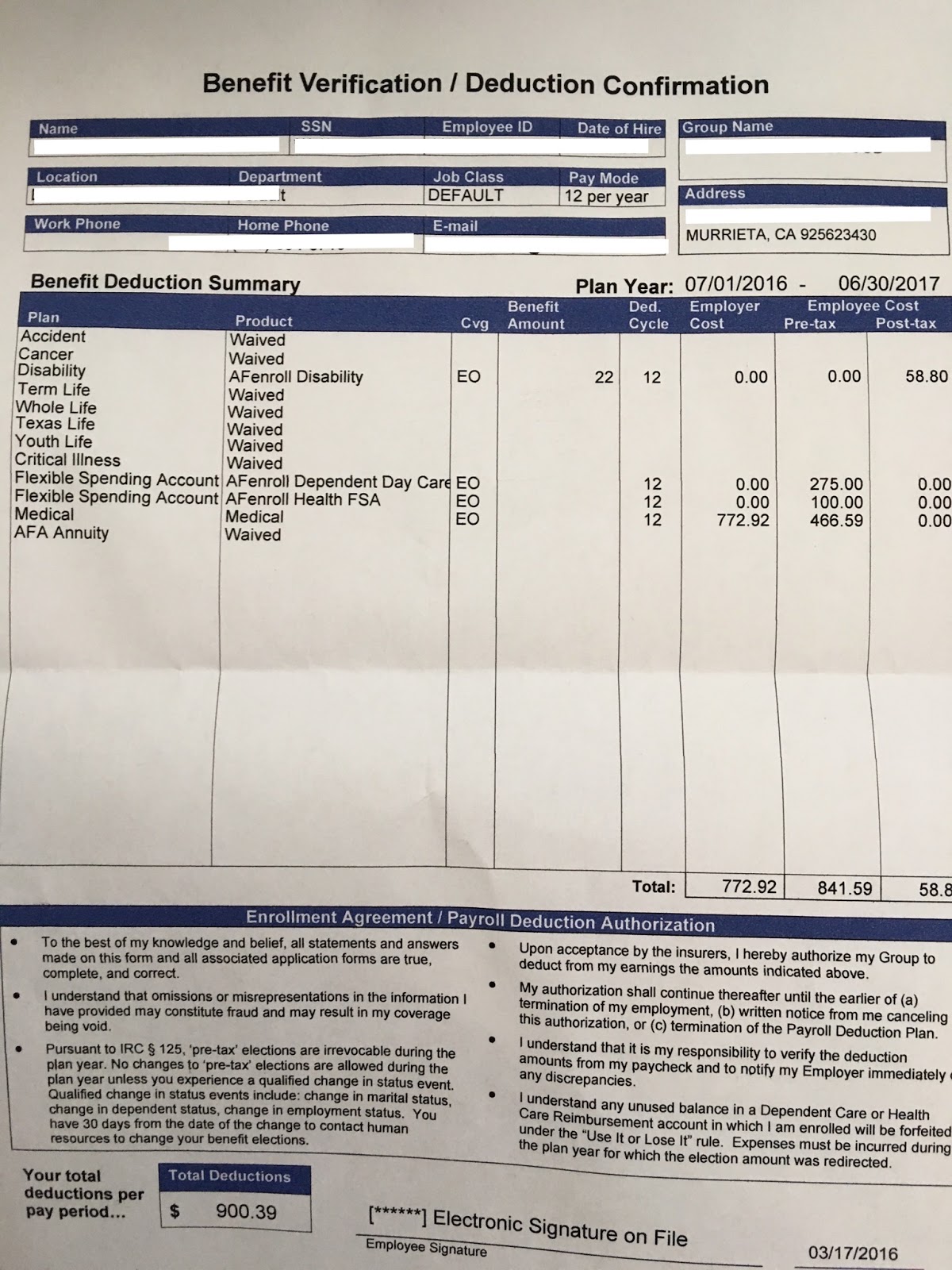

American Fidelity sells Accident, Cancer, Disability, Term Life Insurance, Whole Life Insurance, Youth Life Insurance and Critical Illness Insurance in addition to a terrible 403(b) product.

Taxing your health insurance benefit is a ploy to get every school district employee to meet one-on-one with an American Fidelity sales rep. American Fidelity even pays for substitute to take over Teacher classes while they meet. Folks, this is nothing short of coercion.

I had the unfortunate problem of having my wife NOT meet with one of these sales reps one year and guess what, the district started taxing our health insurance benefit. A benefit that everyone receives for free and almost no one would refuse is suddenly taken away because we refused to meet with a person selling crappy insurance products during school hours.

I asked the district why anyone would want their health insurance taken out after-tax and the response was "There are employees who do not pre-tax the premium due to social security credit needs." This is not only a lame excuse, it's not true. Pre-tax health insurance has no affect on social security credits. Even if this were true, it's a tiny minority of employees who would want their health insurance taken out after-tax, they should be the ones required to meet with the agent (though a simple form would take care of it).

I believe the only reason the district forces every employee to meet with an American Fidelity sales agent is so that they can guarantee American Fidelity a steady flow of leads to sell their crappy products and make up the costs of running the Section 125 plan.

To which my response is "Wait, that's legal?".

Every year my wife has to do the American Fidelity dance...leave her classroom in the middle of the day to march up to the front office to meet a sales agent who has no interest in protecting her best interest, solely to say "please deduct my health insurance on a pre-tax basis" and change my Section 125 elections (we can't do this online...?).

This year was interesting because the sales agent didn't even ask her if she wanted her health insurance premiums taken out pre-tax, my wife reminded the agent that she wanted her premiums pre-tax and the agent said "we already took care of it!". Even the agents know it's a ploy and have it automatically marked pre-tax and they don't even take the time to ask otherwise. If that's not proof of a sales scam, I really don't know what is.

School Districts everywhere are feeding their employees to the wolves simply to pay for a program that most employees would gladly pay for out of pocket (we paid $6 per paycheck for our Section 125 plan at another district). This practice needs to stop and the state insurance commissioner needs to look into these sales tactics.

Don't believe me, here is the receipt from my wife's meeting yesterday. I also have proof of when our benefits were taken out after-tax.

This has to stop. This is not ethical and it certainly shouldn't be legal.

Scott Dauenhauer, CFP, MPAS, AIF (This is an opinion piece)